By Michael Msika, Bloomberg Markets Live reporter and strategist

Strategists are bemused by the rebound in European equities since mid-March, expecting the sustained campaign of interest rate hikes to eventually stall the rally.

They are sticking to their gloomy outlook for the rest of 2023, unconvinced by a 10% advance in the Stoxx Europe 600 so far. The benchmark index is set to fall to 450 points by year-end, according to the average of 15 forecasts in a Bloomberg strategist survey, implying a drop of 4% from Friday’s close.

“Monetary policy has been tightened by the sharpest pace in 40 years, which is resulting in a sharp deterioration of credit and monetary conditions,” says Bank of America strategist Milla Savova. “We expect this to lead to recessionary growth conditions over the coming months, which, in turn, would be consistent with a meaningful widening in risk premia.”

The BofA strategists expect earnings forecast downgrades to add to the headwinds, cutting their year-end target for the Stoxx 600 to 410 from 430 last month, implying nearly 13% downside from here. For Savova and her team, the low point for stocks should come early in the fourth quarter, when the economic cycle is expected to bottom, dragging the benchmark to as low as 365.

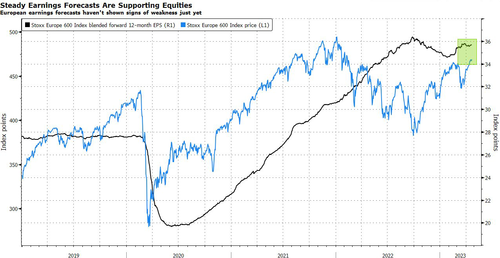

European equities have recouped all the losses induced by the banking turmoil in the US and the collapse of Credit Suisse. The Stoxx 600 surged to the highest since February 2022 this month, buoyed by an economic recovery in China, and rapid intervention by authorities to contain the banking crisis. The trouble is that manufacturing data for the continent have continued to deteriorate, while inflation remains too high for central banks to stop hiking rates.

The largely downbeat assessment from sell-side strategists is mirrored by the actions of the investment industry. According to the BofA European fund manager survey in April, 70% of investors expect weakness in the region’s equity market over coming months in response to monetary tightening, up from 66% last month. Meanwhile, 55% see stocks heading lower in the next 12 months, up from 42%. Sticky inflation leading to more central bank tightening is seen as the most likely cause of a correction, followed by weakening macro data, the survey showed.

While most strategists in our survey have stuck to their forecasts or slightly adjusted their view downward in the past month, some found justification for an increase. State Street Global Advisors, for instance, raised its target to 475 from 455, although this only implies limited upside for the rest of the year.

“The financial contagion from the banking sector in March had been very well contained so far and markets have rebounded,” says Frederic Dodard, head of EMEA portfolio management at State Street Global Advisors. The firm continues to favor European equities over other regions, but sees a modest risk from negative guidance and additional downgrades to companies’ 2023 and 2024 earnings forecasts, he added.

The first-quarter earnings season has kicked off with some positive surprises, and there could be more to come. But this shouldn’t be extrapolated as a signal of stronger stock performance, according to JPMorgan strategists. Low profit expectations have been easy for companies to beat, while the numbers also got a leg up from economic activity that was better than in the first-quarter of 2022, they argue.

“The question is whether the stocks will rally much further on the back of beats, post an already strong rally,” say strategists led by Mislav Matejka. “We advise to use any strength on the back of positive first-quarter results as a good level to reduce from.”

Loading…