Well that was a week…

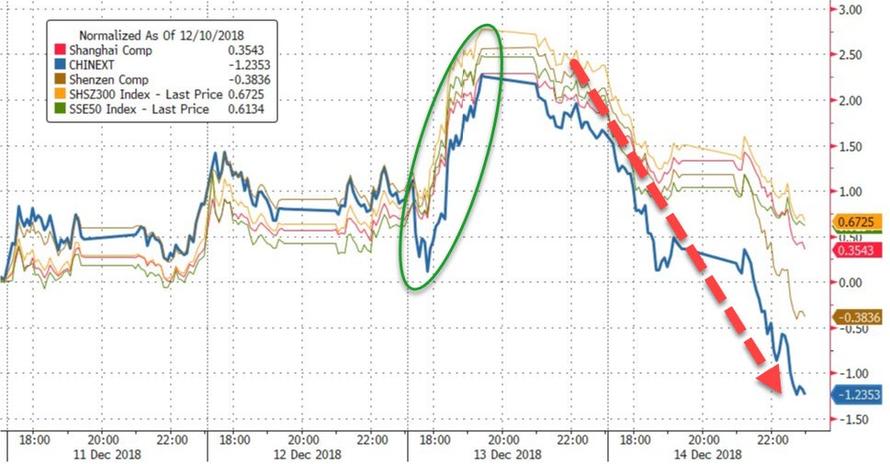

Despite The National Team’s efforts on Thursday, the week ended ugly in China…with CHINEXT (China’s small cap/tech heavy index) ending red after terrible economic data hit overnight…

European stocks ended the week higher, despite an ugly Friday…

And after a strong start which prompted every media type to claim the bottom is in, Thursday and Friday were a bloodbath…

The S&P 500 closed at its critical 2,600 support level…

US Small Caps broke to fresh 2018 lows – to their lowest since Sept 2017…

6th day of “sell the fucking rip” in a row…

Year-to-Date, all the majors except Nasdaq are back in the red…

All the major US equity indices are in correction (down 10%) or worse…

-

Dow -10.5% from highs

-

S&P -11.3% from highs – lowest weekly close since March 2018

-

Nasdaq Comp -14.6% from highs

-

Trannies -17.8% from highs – Nov 2017 lows, worst 2-week drop since Aug 2011

-

Russell 2000 -18.5% from highs – lowest since Sept 2017

The number of bulls in the AAII survey of U.S. retail investors suffered its biggest one-week decline since 2010 this week. In aggregate, sentiment is still nowhere near the overly pessimistic extremes that typically develop at major lows, but this freak out in the retail channel is a constructive development.

The S&P Banks and Financials indices are both down over 20% from their highs (in bear market)…

For The Big 4 Bulge Bracket Banks, December has been a bloodbath…

FANG stocks gave back the mid-week squeeze gains (down 23% from their highs)…

AAPL was hammered (down 29% from the highs)…so much for Monday afternoon’s panic-bid that CNBC crowed so loud about…

And JNJ crashed most since 2002 as cancer-causing talc headlines hammered the stocks down below its 200DMA (and dragged the Dow down 100pts alone). JNJ lost almost $35 billion market cap…

Tesla stock had another great week… but TSLA bonds didn’t – who do you believe?

Breadth is getting extremely weak with just 24% of all NYSE stocks now trading above thei 200DMAs…

And the S&P’s put/call ratio has crashed…

And the market’s implied correlation is soaring (implying traders using macro overlays to hedge and not being idiosyncratically careful)…

As soon as Tuesday/Wednesday’s short-squeeze ran out of ammo, the week went a little pear-shaped…

Credit markets actually rallied on the week in IG and HY spreads…

But Leveraged Loans were a bloodbath…

And stocks have a long way to catch down…

Treasuries rallied on the day as stocks stumbled with 30Y back to unchanged on the week…

And if equity markets are right, bond yields have a long way to fall…

2s5s remains inverted…

And as far as next week’s Fed meeting, odds of a hike have slumped (very weak this close to a meeting)…

And the market is now pricing in just 9.5bps of hikes in 2019, and a 10bps cut in rates in 2020…

The Dollar Index soared again today (best week since September) – touching its highest since May 2017 intraday…

Offshore Yuan roundtripped on the week

Cable plunged again (5th week in a row) to the lowest weekly close since April 2017… despite a rally on May’s confidence vote

Cryptos had another ugly week with Bitcoin Cash crashing 25% …

Despite the terrible China data, only copper ended the week higher in commodity-land as a strong dollar dragged down PMs and WTI algos went wild…

After two weekly gains (following 7 weeks straight down), WTI resumed its down trend this week testing back to a $50 handle…

Gold was lower in USDollars and in Yuan…

Finally, we note that after this week’s rounds of economic data disappointments, all of the major economies in the world are now in negative surprise territory (but ironically the US is least worst for now)… The Global macro surprise index is at 6-month lows

And this is probably nothing to worry about – the world’s most systemically important banks continue to collapse…