Well, we’ve crossed a historical landmark.

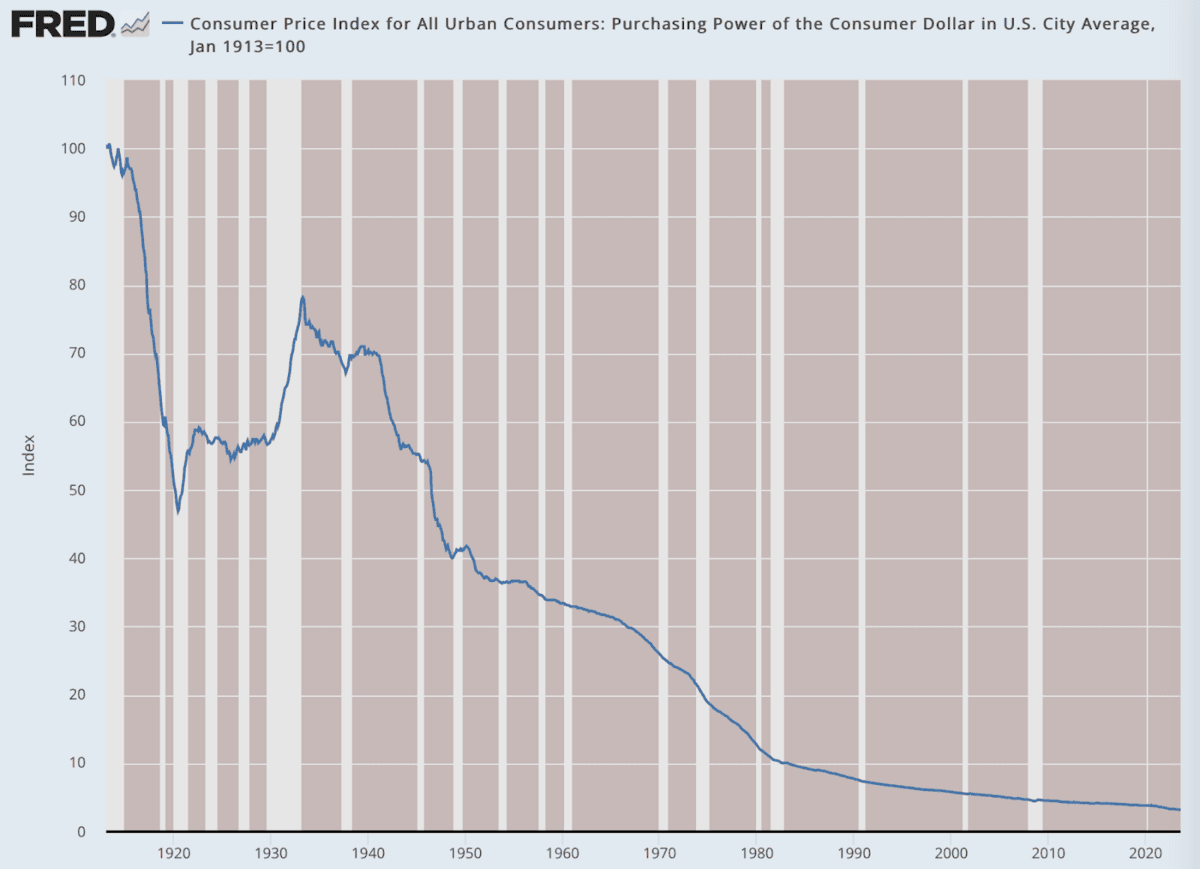

From the founding of the Federal Reserve to the present, the United States has experienced fully 3,000 percent inflation. That is to say, the value of the single dollar in terms of goods and services has been systematically reduced since 1913 to only 3.2 cents today.

This is surely one of the great failures of central management in U.S. history. The Federal Reserve system has not worked. Instead of being a guardian of the dollar’s value, it has presided over its near destruction.

To be sure, you could say that the Fed was never supposed to curb inflation but rather give the United States a more flexible monetary policy than had previously existed. Under the older system, the banking system was unable to adapt to changes in money demand, unstable, prone to bouts of bank failures, and vulnerable when faced with localized investment frenzies. The point of the Fed was merely to reduce bank failures, curb “wildcat banking,” and provide more stability.

All of that is true. The Fed certainly has given us a flexible monetary system. It’s also true that when the Fed was founded, there was no such thing as “monetary policy” as we currently understand the term. Keynesian economics had not yet been invented. There was nary a thought of manipulating the money stock to reduce unemployment or curb macroeconomic business cycles. Economics as it was then understood could not conceive of such a thing.

“The Federal Reserve Act … did, however, require the Reserve Banks to maintain gold reserves equal to specific percentages of their outstanding note and deposit liabilities. Implicitly, this requirement was intended to limit the amount of currency and loans the Fed could issue and thus serve as a brake on inflation.”

This is correct. The founding generation were not all ruling-class racketeers. Some were old-school sound money advocates who favored the gold standard and were extremely wary of populist demands for looser money. The money debates of the 1880s and 1890s profoundly affected them. They came out decidedly for strict standards of accountability. They did not want the banking system involved at all in financial schemes, which is why signing up to be part of the system came with all sorts of regulatory strings attached.

The problem is that very quickly after its founding, the pressure was on for the Fed to behave like a national bank, which is to say be a provider for liquidity for government itself. As one might expect, the Fed accommodated that demand. It was supposed to be a temporary measure to fund the expenses of the Great War.

This was the problem with the deal from the beginning. The government essentially created a banking cartel, in exchange for which this cartel had to pay obeisance to its benefactor, the federal government. That’s when its power to buy and hold U.S. debt with newly created money started to be deployed.

Just seven years after its founding, the disaster became obvious as the dollar had already lost half its purchasing power. But that was only the beginning of the trouble. The other problem was all the distortion into industrial structures that was wrought by new money. Monetary expansion generates booms that are followed by busts. They were not dissimilar to what existed in the pre-Fed times but these were expanded from regional problems to national ones.

The inflation of the late 1910s was in fact followed by a dramatic depression of 1920–21. The one good thing we can say about that period is that the Fed managers were done with politics at this point. They simply let the depression come, doing nothing at all to alleviate the downturn. That was exactly the right path. Sure enough, the recession ended in due course. The country got back on a growth path.

However, the damage caused by the previous expansion was not yet completed. By the second half of the 1920s, monetary creation got out of hand again, pumping up the stock market until it crashed in 1929, causing financial wreckage all around. This time, the Fed was called upon to act. There were some half-hearted attempts to cut interest rates but the forces of deflation were far too powerful.

In 1932, Franklin Roosevelt ran on a platform of balancing the budget, repealing alcohol prohibition, and otherwise repairing the fiscal damage caused by the Hoover administration. But once he took office, he quickly pivoted. He closed the banks and issued an executive order to confiscate gold, and devalued the dollar. This set the Fed once again on a bad course, eventually finding itself in the position of providing liquidity for yet another war.

This has gone for a century, with the Fed promising to be the fix of the problems that have been caused by its own monetary policies. Notice, however, that they never take responsibility for the inflations and cycles they cause but instead wear the mask of being the answer to all our problems.

Two presidencies of welfare and warfare after the war led to another bout of Fed activism that eventually created the terrible hyperinflation of the late 1970s. That was a real turning point for American prosperity. Families that once got by just fine on one income had to move to two, the value of savings was gutted, and the dollar was hammered once again.

Looking back now, the years 1982 to 2019 seemed like a time of relative stability in Fed policy. Beneath the surface, however, truly wicked things were happening. The response to the financial crisis of 2008 was to drive interest rates to zero while incentivizing the banks to keep newly printed money off the streets. That kept inflation at bay but introduced astounding distortions in industrial structures. It was this that unleashed the imperiums of Big Tech, Big Media, and corporate and government bloat in managerial positions.

As for 2020, that was a disaster for the ages, the single worst policy decisions by the Fed in its entire history. In the course of a few days, the Fed completely eliminated reserve requirements, introduced a huge range of new lending systems, bought every dollar of debt that the Treasury could create, and, over two years, unleashed the terror of $6.5 trillion on a demoralized public that was initially excited for the benevolence.

That charity turned to dust once the inflation started. Now it’s all gone and we are dealing with three straight years of real declines in median family incomes.

And here we are today after 110 years of promises that have faded into nothingness. It’s time for the Fed to accept responsibility for this mess. They of course will not.

What to do? Unplug the whole machine. Return to sound money. Make the banking and financial system function like normal businesses without their benefactor the Fed forever saving them from their own mismanagement. Yes, that means abolishing the Fed completely. It has utterly failed.

This should happen before times get worse. We know from a long history that the Fed cannot be trusted with managing the nation’s (and the world’s) money stock. It has been the handmaiden of government growth, declined living standards, and relentless economic instability. If we had a modicum of respect for the evidence before our eyes, the Fed would be shut down today.