Concerns about rising inflation, and the Fed hiking rates to contain it, have reversed rather dramatically.

As Bloomberg’s Edward Bolingbroke observes, after months of consensus trades that the Fed’s easing cycle will end in 2026, traders in US futures and options markets are suddenly piling on bets that the Fed will continue cutting rates well into next year instead of raising them.

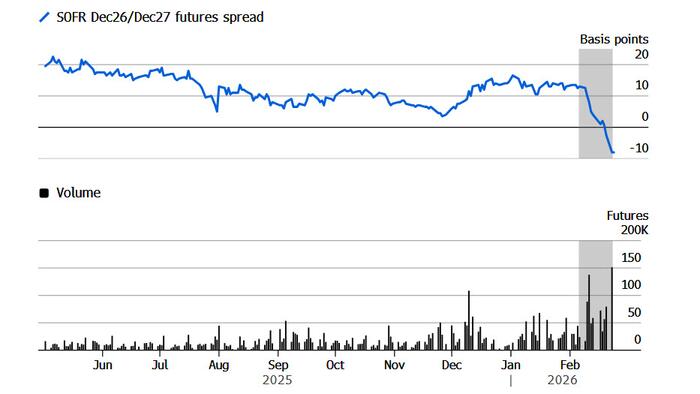

As shown below, the key spread linked to the SOFR (the Secured Overnight Financing Rate) which track expected Fed policy, have becoming deeply inverted in the past week, a sign that traders are starting to price a more prolonged easing cycle. The 12-month December 2026 to 2027 SOFR spread dropped into negative on Friday with the inversion deepening on Tuesday to minus 8 basis points, in a sign that investors have flipped from pricing hikes in 2027 to pricing cuts.

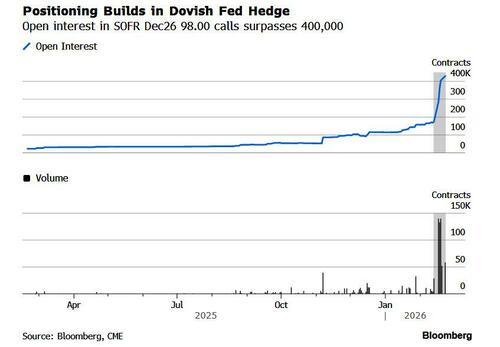

In the SOFR options market a similar dovish theme is observed for trades that are hedging (or encouraging, depending on how one views the role of options) the prospect of multiple rate cuts this year. Those trades picked-up again on Tuesday with one position that’s looking to hedge for the policy rate falling to as low as 2% by the end of the year growing in size.

Open interest in the December 98.00 calls ballooned to more than 400,000 this week. A record amount of just over 150,000 calls traded in the 12-month spread over Monday’s session, while the total open interest of SOFR Dec26 98.00 calls soared above 400,000 amid the trading frenzy. For context, the swaps market is currently pricing a Fed rate of around 3.1% – or just over two 25-basis point cuts – by year-end, some 110 basis points above the options strike price.

Until mid-February, traders were betting that the central bank would resume hiking rates in 2027 after two quarter-point reductions by the end of this year. However, the ongoing wipeout of Software stocks and the growing debate around the impact of artificial intelligence on the labor market is leading them to reassess this outlook. On Tuesday, Fed Governor Lisa Cook warned that the central bank may not be able to counter rising unemployment driven by the adoption of AI.

Which, of course, leaves fiscal policy as the only recourse to provide a safety net for the millions of soon-to-be-unemployed white collar workers displaced by chatbots. And, fiscal policy needs to be funded by brrrr, which means sooner or later the Fed will have to print again, just as we said back in 2024 in a 22-word tweet which effectively previewed and summarized that 7000 word Citrini essay far more eloquently.

Market pricing so much AI success, it will need to leave about 100 million people without a job.

Bring on the UBI

— zerohedge (@zerohedge) January 24, 2024

But we’ll cross that money printer when we get to it: for now, what’s important is that the flattening move in SOFR spreads accelerated sharply since the end of last week, just as AI disruption fears took a toll on a swath of stocks, setting off a rally in long-dated Treasuries and raising recession odds among multiple brokers..

Gennadiy Goldberg, head of US rates strategy at TD Securities, told Bloomberg that “there has certainly been a bit of repricing for lower yields after the Fed hits terminal, with the market penciling in a more gradual drift higher in yields.”

“That could be driven by uncertainty regarding the impact of AI on the labor market, but fluctuations in longer-dated Fed expectations tend to be quite significant, making it difficult to read into them,” he added.

And indeed, “the question is how is AI going to be inflationary and maybe the long end of the curve is sniffing all of this out,” said Jack McIntyre, portfolio manager at Brandywine Global Investment Management. “The only inflationary aspect of AI is the building out of data centers and the associated energy needs, and that is known.”

Market positioning for prolonged rate cuts is also becoming evident in treasury curve metrics: the 2- to 5-year spread reached the flattest levels since the start of December on Monday, while the richening of the 2s5s30s butterfly was the biggest one day move seen in six months, driven by outperformance in the belly of the curve.

While many herd-following investors will be caught offside by this latest twist in Fed pricing, one fund manager who has called it correctly so far is David Einhorn: two weeks ago, the co-founder of Greenlight Capital said he has bought Secured Overnight Financing Rate (SOFR) futures on expectations of a rally if the Fed lowers borrowing costs more aggressively.

“I think one of the best trades out there right now is betting on more cuts this year than expected,” Einhorn said on CNBC On Feb 11 . “I think by the time we get to the end of the year, it’s going to be substantially more than two cuts.”

And not only this year, but next year too.

He made the comments after a better-than-expected jobs report prompted traders to pare back their bets for Fed cuts this year, to just about two quarter-point moves.

Einhorn said Warsh, whom President Donald Trump has picked to succeed current Fed Chair Jerome Powell, is likely to deliver what the president wants: Lower borrowing costs. Trump has relentlessly pushed Powell to lower rates, a move that would help reduce interest costs on US government debt.

Einhorn said Warsh, a former Fed governor, could convince his colleagues to adopt his view that rising productivity will create room for easier monetary policy – even if the economy is strong. Since then, the term “rising productivity” has rapidly become synonymous with mass future layoffs and so here we are.

“He’s not being brought on to hold the rates at a steady rate,” Einhorn said. “He’s going to argue we can cut even if the economy is running hot.” Suddenly, the market agrees with him.

Loading recommendations…