Tl;dr: Bloomberg macro strategist, Michael Ball, warned that President Trump’s urging of Iranians to overthrow the government gives Saturday’s US and Israeli strikes on Iran the potential to usher in a more prolonged higher-volatility era rather than being a one-off tradeable shock.

Traders will be closely watching for updates on crude production and shipping disruptions, and any spike in oil will move across global rates and FX and eventually weigh on equities – but Trump’s post-strike comments make it harder for markets to assume this is one and done.

A limited strike would likely see the usual pattern:

Crude and gold spike, equities wobble, then volatility compresses if production is unaffected and Strait of Hormuz flows keep moving, leading the risk premium to ebb quickly.

But a longer-term campaign framed around leadership removal is different.

It will stretch the uncertainty window, raise the probability of wider tail risk outcomes, keep oil prices elevated and volatility high and force broader risk premiums to reflect a more uncertain growth and inflation backdrop.

* * *

Submitted by QTR’s Fringe Finance

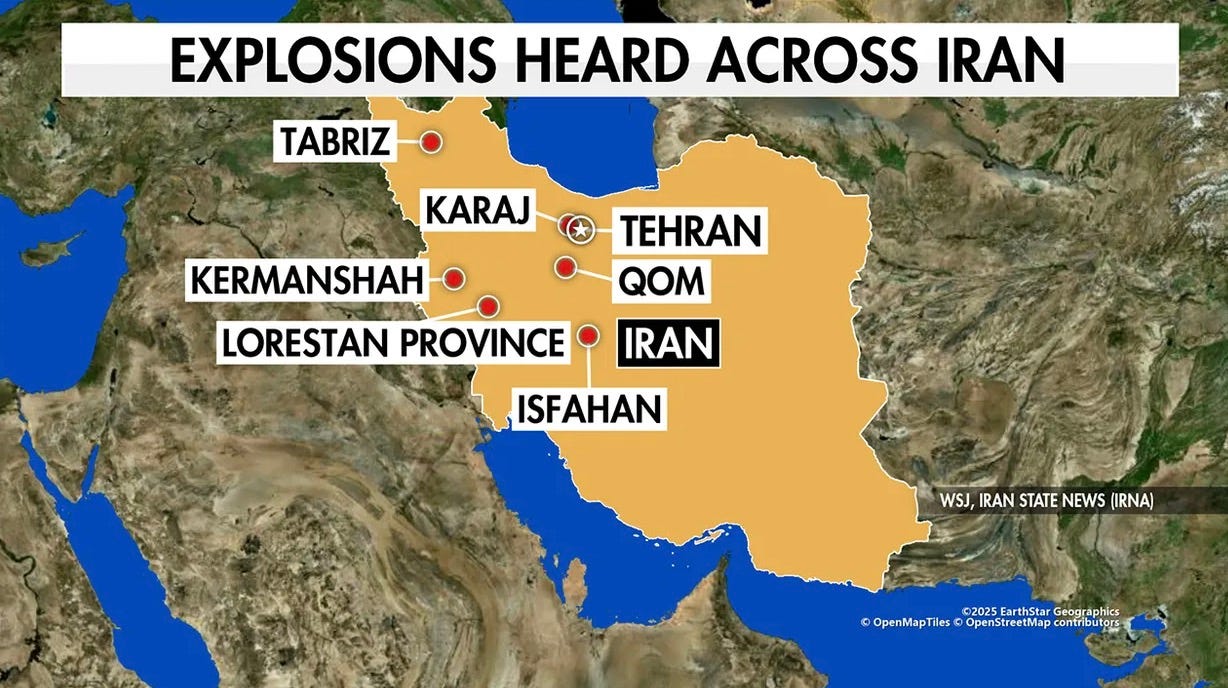

Most of the U.S. woke up today to news that that the U.S. and Israel have started “major combat operations” and a broad military campaign against targets across Iran.

Also it looks like we have an answer about the “mystery” SPY put buyers and the super aggressive gold and silver call buyers into the close last week.

Someone was obviously in the know that full-scale military action involving Iran was about to kick off Friday night and was positioning ahead of it.

Anyone who tells you the options market can’t telegraph news or hint at where the market is headed isn’t paying attention.

Order flow doesn’t predict everything – but sometimes it absolutely signals that something big is coming.

The operation against Iran reportedly began with strikes in Tehran and other strategic locations late last night/early this morning. President Donald Trump urged Iranian civilians to take shelter during the attacks, but also made unusually direct comments suggesting that once operations conclude, Iranians should reclaim control of their government. The framing went well beyond nuclear concerns and referenced decades of hostility between Washington and Tehran since the 1979 revolution.

Initial targets reportedly included areas associated with Iran’s Supreme Leader, Ayatollah Ali Khamenei, though it was not immediately clear whether he was present. Smoke was seen rising over parts of Tehran as the strikes unfolded.

According to various live reports (AP, CNN, Bloomberg) up until this morning, Iran responded quickly. The Revolutionary Guard announced it had launched drones and missiles toward Israel in what it described as an initial wave of retaliation. Air raid warnings sounded across Israel as the military moved to intercept incoming fire.

The stated rationale from Washington and Jerusalem centered on escalating tensions over Iran’s nuclear program and missile capabilities. U.S. naval assets had been repositioned in the region in recent weeks as diplomacy stalled. Israeli Prime Minister Benjamin Netanyahu characterized the joint action as necessary to eliminate what Israel sees as a direct and existential threat.

The regional fallout has been swift. Iraq and the United Arab Emirates closed their airspace. Sirens were reported in Jordan. Bahrain said a missile targeted the headquarters of the U.S. Navy’s Fifth Fleet. Explosions were reported in Qatar. Syria later shut down portions of its southern airspace. Several major airlines suspended flights as a precaution.

European leaders issued a joint appeal for restraint, emphasizing the need to prevent further escalation and protect civilians. They stressed the importance of nuclear safety and adherence to international law while noting that the European Union has long pursued diplomatic efforts alongside sanctions targeting Iran’s leadership and Revolutionary Guard. EU officials said they are coordinating with member states to assist citizens in the region.

Meanwhile, Iran’s Revolutionary Guard said it had struck multiple facilities in retaliation, including U.S. installations in Bahrain, Qatar, and the UAE, as well as military targets in Israel.

Ayatollah Khamenei had not made a public appearance in the days leading up to the attack and had reportedly been moved to a secure location during prior hostilities. His current status has not been confirmed publicly. According to a person familiar with the planning, the operation had been coordinated between the U.S. and Israel for months and is expected to continue for several days.

So what does it mean for markets on Monday?

The way I see it, there are two very different paths that are possible here.

One path is that this becomes a non-event by Monday morning. We have precedent.

The U.S. military operation ordered by Donald Trump against Venezuela occurred over the weekend in early January, rather than on a weekday, and involved strikes in and around Caracas and the capture of President Nicolás Maduro.

Markets reopened on the following Monday, and major stock indexes, including U.S. equities and energy shares, were generally steady to higher as investors weighed the news and focused on the implications for oil-related sectors and broader fundamentals rather than selling off sharply in response to the weekend geopolitical event.

In those instances, traders ultimately treated the events as tactical and contained rather than the start of prolonged war. If investors conclude that objectives are narrow, retaliation is limited, and oil flows remain uninterrupted, markets could interpret the move as decisive rather than destabilizing.

In that scenario, dip buyers step in, volatility fades, energy spikes briefly, and by midweek the narrative shifts back to earnings, AI, and Fed policy.

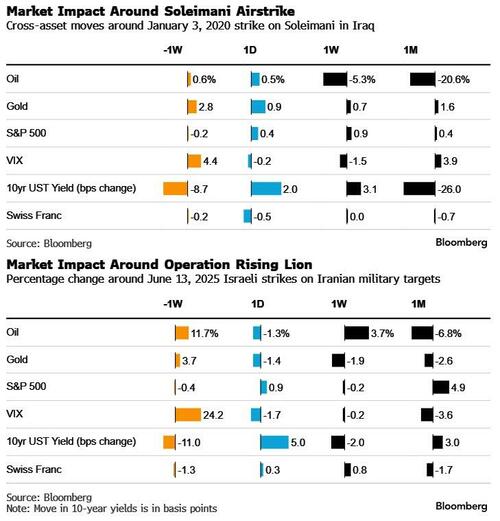

Relevant precedents include the air strike to take out Qassem Soleimani in January 2020, and last year’s extensive Israeli strikes as part of Operation Rising Lion and US strikes on nuclear sites in Iran that comprised Operation Midnight Hammer.

If anyone knows the “I’m long gold and silver at the right time, futures have skyrocketed but by the time the cash open comes they’re already red” scenario, it’s me.

It happened the last time Israel attacked Iran last year — futures were crushed overnight but by the next morning’s cash open, rhetoric had softened and the market had already recovered.

But there’s still always the “other” scenario, too: escalation, both geopolitically and financially.

A worst-case outcome would involve a drawn-out regional conflict marked by heavy missile exchanges and the activation of Iranian proxy groups across Lebanon, Iraq, Syria, and elsewhere. Fighting could spread across multiple fronts, potentially pulling in additional regional actors and forcing deeper U.S. military involvement. Iran could attempt to disrupt shipping through the Strait of Hormuz or target regional energy infrastructure, creating a meaningful shock to global oil supply. Even temporary disruptions could push crude sharply higher, intensify inflation pressures, and rattle global risk assets.

A prolonged conflict could destabilize the Iranian state itself, creating internal fragmentation, humanitarian crisis, or a power vacuum. Alternatively, a regime under severe pressure might accelerate nuclear development as a deterrent. Either direction introduces multi-year instability.

The economic consequences would likely include higher energy costs, rising shipping and insurance expenses, and a broad tightening of financial conditions — all while global growth is already fragile.

There is also an ugly scenario that I don’t think is extremely likely, but needs to be taken very seriously.

As I wrote Friday, the market was only just beginning to acknowledge cracks in private credit. Bank stocks were being sold aggressively.

That matters because private credit has been one of the pillars of liquidity supporting risk assets over the past several years.

If stress there deepens, it can spill into broader credit markets quickly.

At the same time, last week’s ugly PPI data complicated the Federal Reserve’s position. Sticky inflation limits how aggressively policymakers can ease if financial conditions tighten. If you combine a Fed that looks constrained, early tremors in private credit, aggressive bank selling, and now the introduction of a serious geopolitical shock, the margin for error to keep a market trading at a Shiller PE of 40x shrinks.

If energy prices spike and inflation expectations rise, yields could climb at the same time growth expectations fall — a stagflationary mix that equities historically struggle with.

That is the type of setup that can turn a contained event into a liquidity event.

And once liquidity events begin, correlations go to one.

Positioning into Monday becomes less about prediction and more about preparation.

My 26 Stocks I’m Watching for 2026 were built with this type of uncertainty in mind. Precious metals names provide a hedge against geopolitical instability and currency debasement. Energy exposure benefits if crude moves higher or supply risk premiums expand. Select emerging markets with commodity leverage can outperform in resource-driven cycles. Consumer staples offer defensive ballast if broader indices wobble.

I’m not scrambling to overhaul that list. The bigger adjustment for people positioned similarly will be mostly mental. You prepare for a range of outcomes.

Green futures because traders assume containment. A sharp red open if oil gaps higher and risk parity funds de-risk. A volatility spike that fades by midday. Or a genuine air pocket if credit markets continue Friday’s mini-bank run and seize up.

This is also a reminder of how quickly narratives shift. On Thursday, the focus was inflation prints and private credit stress. By Saturday morning, we are discussing potential regional war that’ll take “days, not hours”, according to U.S. officials. Markets are reflexive and forward-looking, but they are not omniscient. Complacency builds quietly during extended rallies, especially when liquidity has repeatedly rescued drawdowns.

Sharp downturns often arrive before policymakers step in. If history is any guide, meaningful volatility tends to precede intervention — not follow it.

And again the larger lesson: things change fast, and they change without notice. Complacency kills, even in markets that appear permanently supported.

Loading recommendations…