A relatively hawkish Fed statement – removing language that it has “gained greater confidence that inflation is moving sustainable toward 2 percent” – was met with a ‘meh’ response by the market, but once Fed Chair Powell started speaking it was clear that the uber-dovish rate-cut trajectory that so many hoped for was a thing of the past… for now.

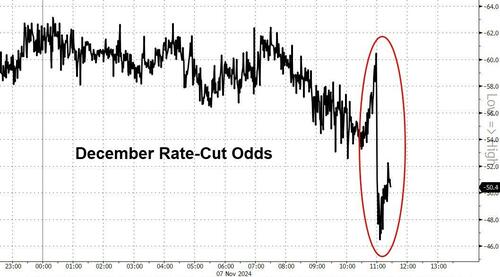

Rate-cut expectations for December stumbled notably…

Source: Bloomberg

During the press conference, The Fed chief notes that while overall inflation has moved closer to the central bank’s goal, core inflation is still “somewhat elevated.”

Powell says the latest inflation report “wasn’t terrible,” but price increases were a little higher than expected.

“We don’t guess, we don’t speculate and we don’t assume.”

Powell says economic activity “has continued to expand at a solid pace,” nodding to strong GDP data and “solid” labor market reports.

“We don’t think it’s a good time to be doing a lot of forward guidance.”

As the Fed gets closer to neutral, it may be appropriate to slow the pace of recalibration, he says.

“It’s something that we’re just beginning to think about.”

Powell says they are not in a hurry to “find neutral.”

Powell, when asked what his plan to deal with stagflation is:

“Our plan is not to have stagflation”

Solid plan, Jay!

Finally, Powell says in the near term, the election “will have no effect” on Fed decisions.

Finally, here’s a more ominous take to all this sudden walking-back of The Fed’s dovishness:

“If inflation is still elevated and the committee risks are roughly in balance, what is the point of continuing to cut?” asks Byron Anderson of Laffer Tengler Investments.

“The Fed gained control of the recession narrative with its supersized cut at the last meeting. If you believe the economy is on good footing, the risks to inflation are increasing with every rate cut they do.

Without a credit crisis emerging, which is not evident at the moment, the greater risk to markets is adding stimulus to an already inflationary leaning environment.

Many will disagree but this was the perfect point for the Fed to pause and reassess the landscape through the end of the year.”

So where did that leave us?

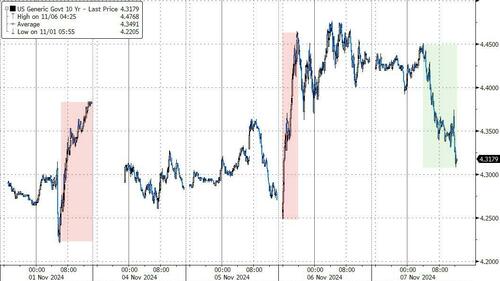

Treasury yields plunged on the day with the belly outperforming (7Y -13bps, 2Y -7bps, 30Y -7bps). That dragged all yields lower on the week…

Source: Bloomberg

It’s been a wild few days in bond-land, between payrolls, the election, and now The Fed…

Source: Bloomberg

The US equity majors were mixed with Nasdaq (and S&P) soaring while The Dow and Small Caps were unable to break out to the upside (with late-day selling pressure pushing Small Caps significantly lower)…

Mega-Cap Tech continued to surge…

Source: Bloomberg

…as the Nasdaq/Small Caps ratio rebounded off the lows of its long-term range…

Source: Bloomberg

‘Trump Trade’ gains continue to hold…

Source: Bloomberg

The post-election, and now post-FOMC VIX collapse continues…

Source: Bloomberg

VIX is back at a critical support level

The dollar slipped lower, back to pre-payrolls levels, erasing most of the election spike…

Source: Bloomberg

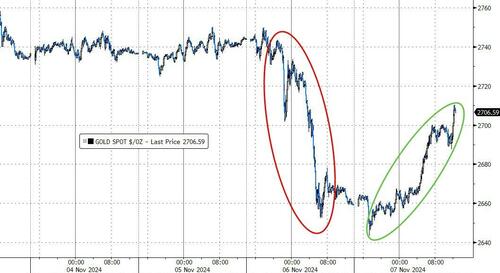

Gold rebounded on the dollar weakness, back above $2700…

Source: Bloomberg

Bitcoin extended its gains to new record highs…

Source: Bloomberg

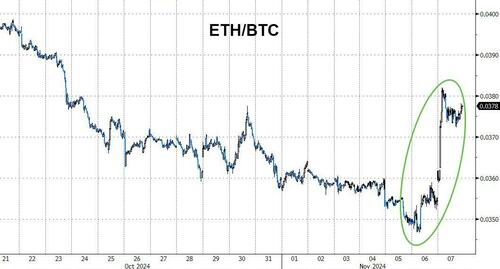

Ethereum also took off today again, topping $2900…

Source: Bloomberg

ETH outperformed BTC bigly today – the biggest outperformance day since May 2024…

Source: Bloomberg

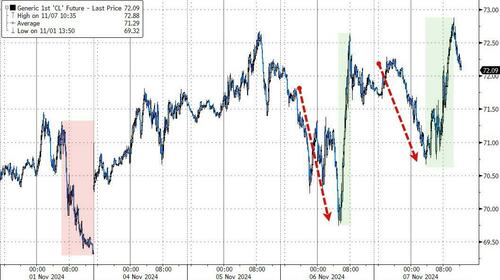

Oil prices dumped and pumped again, with WTI ending back above $72…

Source: Bloomberg

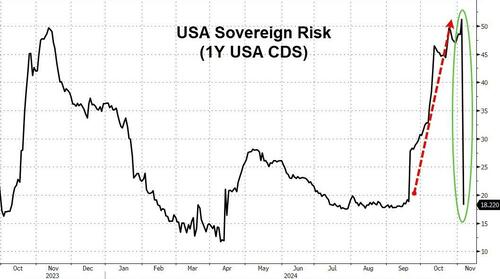

Finally, this is a stunner… it appears the market was using short-dated USA sovereign CDS to hedge the possibility of Kamala winning…

Source: Bloomberg

Since Trump’s Red Sweep, USA Sovereign risk has collapsed!!!

Loading…