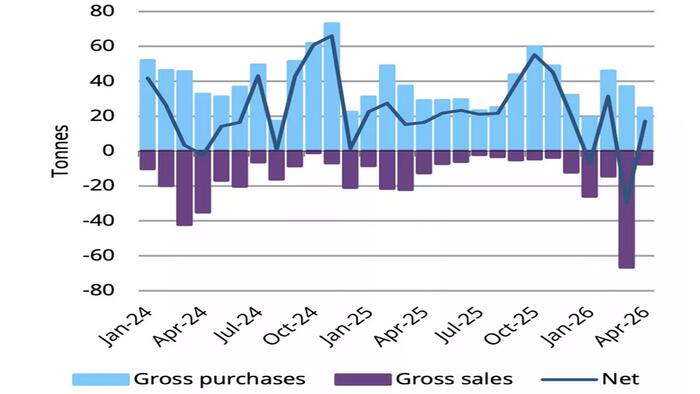

First the good news: according to the latest World Gold Council update, central banks, a key pillar of the bullish case for gold, have returned to adding holdings in April after notable selling in March sent the price of the precious metal tumbling. The 17 ton purchase represents a turnaround from steep sales in March, which at nearly 30 tons were the largest monthly gold sales in years, driven almost entirely by Turkey. Poland remained the top buyer in the month, while China accelerated its pace of purchases.

According to WGC, Poland remained be the top buyer in the month (14t), while China intensified its pace of purchases: its 8t net purchase was the highest since December 2024 and extends its current buying run to 18 consecutive months. The Czech Republic shows similar consistency in purchases, having bought 3t in April, its 38th consecutive monthly purchase. Meanwhile, Russia continues its sales streak this month (6t), with y-t-d sales of 22t.

Reported activity in April and y-t-d was concentrated in:

- National Bank of Poland drove much of April’s buying activity, having bought 14t. This brings Poland’s y-t-d gold purchases to 45t with its gold reserves at595t or about 30% of its total reserves.

- People’s Bank of China added 8t to its gold reserves during the month, highest since December 2024. Official gold reserves now stand at 9% of total reserves or around 2,322t. China has been consistently purchasing gold over the past 18 consecutive months.

- Czech National Bank’s modest but consistent 2t net purchases in April brings its gold reserves to 79t or 6% of its total reserves.

- Meanwhile, Central Bank of Uzbekistan sold 1t this month, though on a y-t-d basis, it remains a net purchaser (24t) and is second only to Poland. Uzbekistan’s reserves make up 88% of its total reserves or around 414t.

- Central Bank of Russia continued it recent streak of net sales for the fourth month with reported April net sales of 6t.

- March’s top seller, Central Bank of the Republic of Turkey reported virtually flat gold reserves in April, with weekly data showing that short-term gold/USD swaps matured in April, leaving only longer-term (1-3 month) gold/USD swaps outstanding. More on Turkey’s recent reserve management operations can be found in our recently published Gold Demand Trends Q1 2026.

- Eastern European and Asian central banks continue to dominate gold purchases with consistent purchases. Over the past 36 months, both regions have purchased 12t and 11t per month on average collectively. Global central banks activity shows average net purchases of 29t over the same period (Chart 2).

Now the bad news: according to Goldman, even as the rebound signals a return to sturdy central bank demand, it’s trending at a fraction of last year’s average pace. Meanwhile, the driver of last year’s tremendous move higher which pushed gold above $5000, has yet to return: the furious ETF buying that characterized the meltup phase in gold, is not there; in fact, ETFs continue to sell as all momentum-chasing liquidity has landed in such areas as chip and memory stocks.

That underscores that the market is currently more focused on the near-term headwinds for the bullion rather than its structural tailwinds.

Meanwhile, with Treasury yields and the dollar grinding higher as the US economy proves surprisingly resilient in the face of elevated oil prices, and with positioning on the back foot, the path ahead for gold remains challenged.