Central Bank ‘Pause’ Panacea Prompts Massive Stock Short-Squeeze, Buying-Panic In Bonds

Tl;dr: Markets melted up after the following folding foursome:

-

Fed‘s Powell says “disinflation” 13 times

-

BOC pausing

-

BOE pausing

-

ECB one more and done, turns to “climate QE”

Most notably, Powell’s “pussying out” of pushing back against market euphoria, drove US financial conditions to their ‘loosest’ since Jackson Hole… where he warned “more pain is coming”, and most presciently to today’s actions: “Restoring price stability will likely require maintaining a restrictive policy stance for some time. The historical record cautions strongly against prematurely loosening policy.”

Source: Bloomberg

The market continued to shift Fed rate trajectory expectations in a dovish direction…

Source: Bloomberg

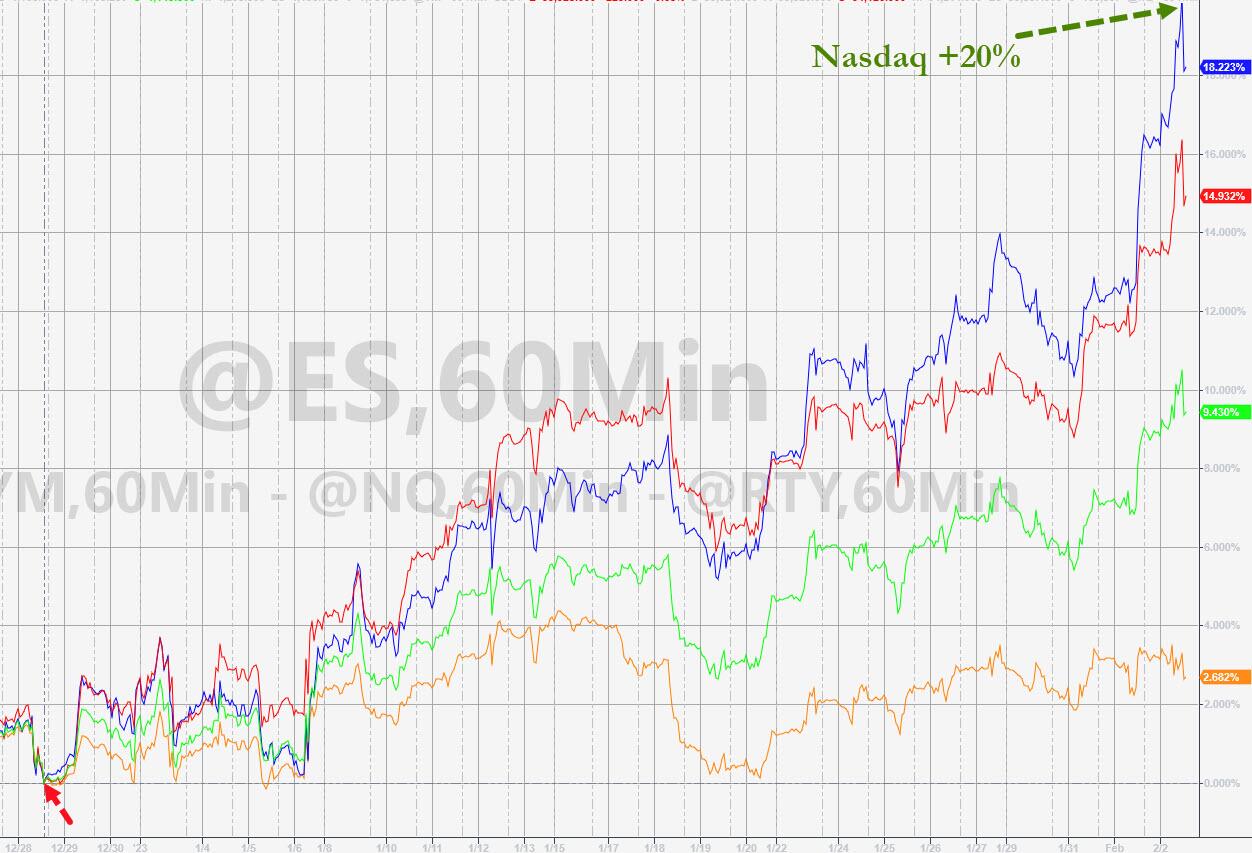

And that ripped stocks higher with Nasdaq leading the charge on the day (but we note that The Dow slipped lower on the day). Stocks all reversed lower together at 1400ET (no obvious catalyst), but the last hour saw the bid return with Nasdaq up over 3% (and The Dow desperately trying to end green)…

From the start of Powell’s presser, Nasdaq is up almost 6%…

The Nasdaq came within a few ticks of being up 20% (a new bull market) from the December lows…

The P/E for the S&P (and Tech stocks) are at their highest since April…

Source: Bloomberg

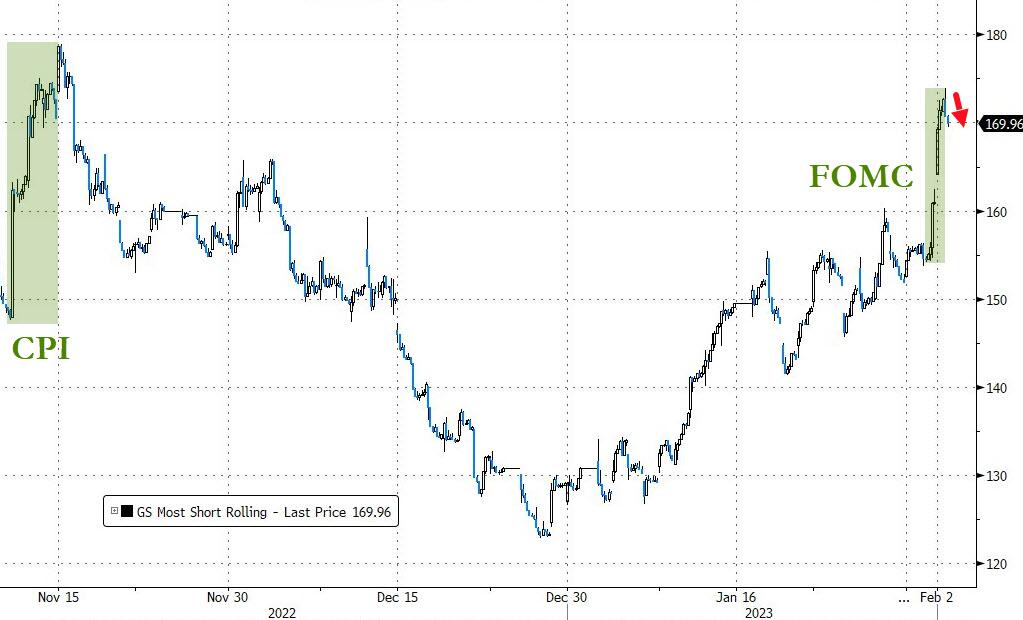

“Most Shorted” stocks were up a stunning 13% from the start of the Powell presser yesterday as the short-squeeze continued through the cash open today. The basket reached all the way up to its post-Nov-CPI squeeze highs before rolling over a little late on…

Source: Bloomberg

Powell achieved the most-impressive short-squeeze yet of this tightening cycle…

Source: Bloomberg

Growth stocks are dominating Value stocks as an ‘easier’ Fed is eyed as imminent (fascinating that the Value/Growth pair reached all the way up to the moment when The Fed last unleashed its easy money spigot)…

Source: Bloomberg

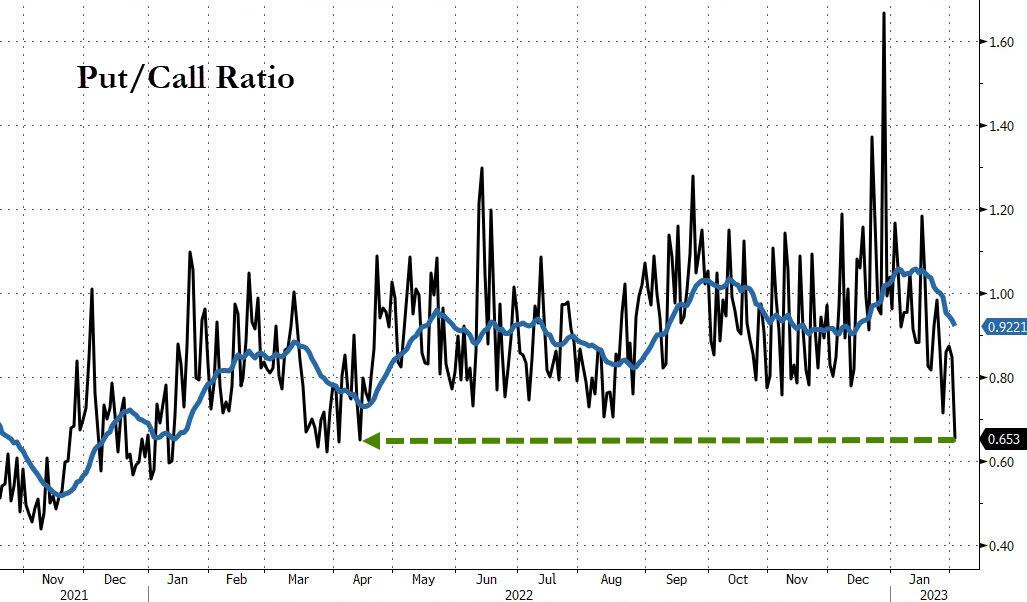

There is no fear anymore apparently as the put-call ratio has collapsed…

Source: Bloomberg

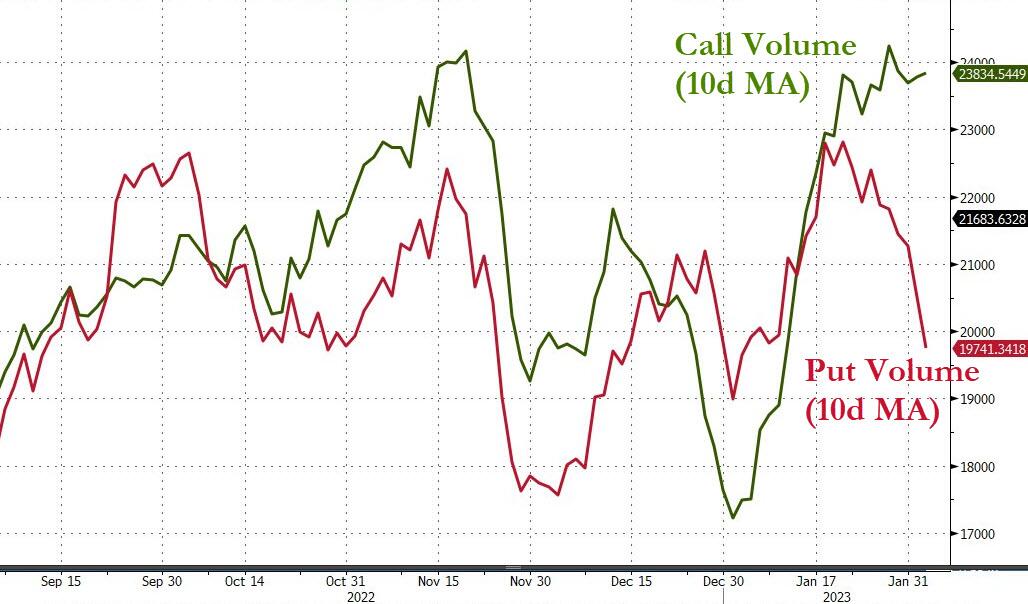

With put volume plunging…

Source: Bloomberg

And no demand at all for downside protection as put vols crashed relative to call vols (upside crash demand jumps)…

Source: Bloomberg

VIX notably decoupled from stocks today, rising up near 19 as stocks rallied…

Source: Bloomberg

As Bloomberg’s Cameron Crise noted, at one point, the SPX was up more than a percent and the VIX was up more than a vol. On a closing basis, that has only happened 16 times since the inception of the VIX in 1990. And on those occasions, the equity market has tended to decline over the ensuing month. The numbers since the Covid era, representing the modern market environment, are even more negative; on average, the SPX has tumbled 2.37% in the week after twin 1% rises.

Yesterday’s Treasury bid extended gains with yields down across the curve and the belly outperforming (5Y -4bps, 2Y and 30Y -1.5bps) but yields reversed higher after Europe closed…

Source: Bloomberg

The 2Y Yield plunged back towards 4.00%, reaching its lowest since October…

Source: Bloomberg

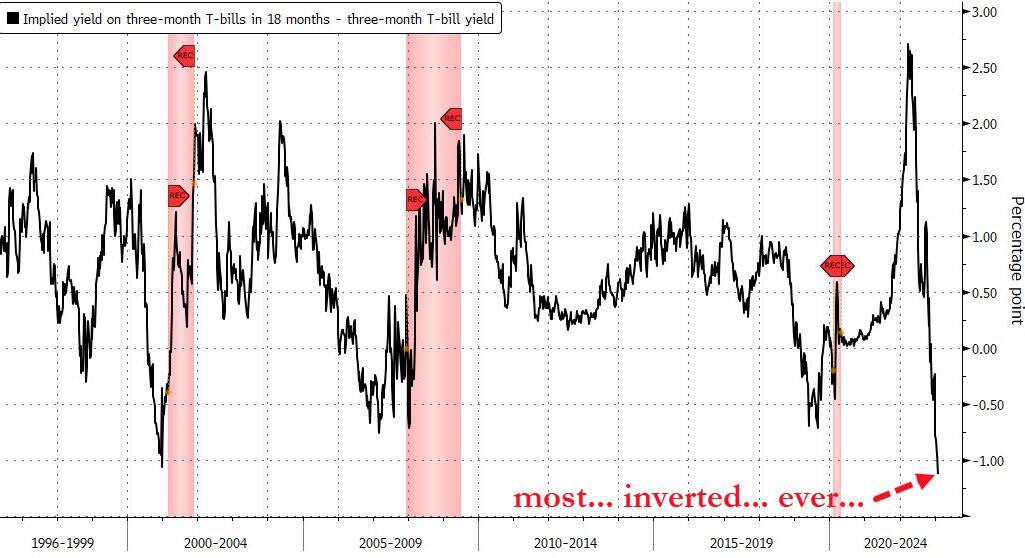

Jay Powell’s favorite yield curve indicator plunged to its most inverted ever…

Source: Bloomberg

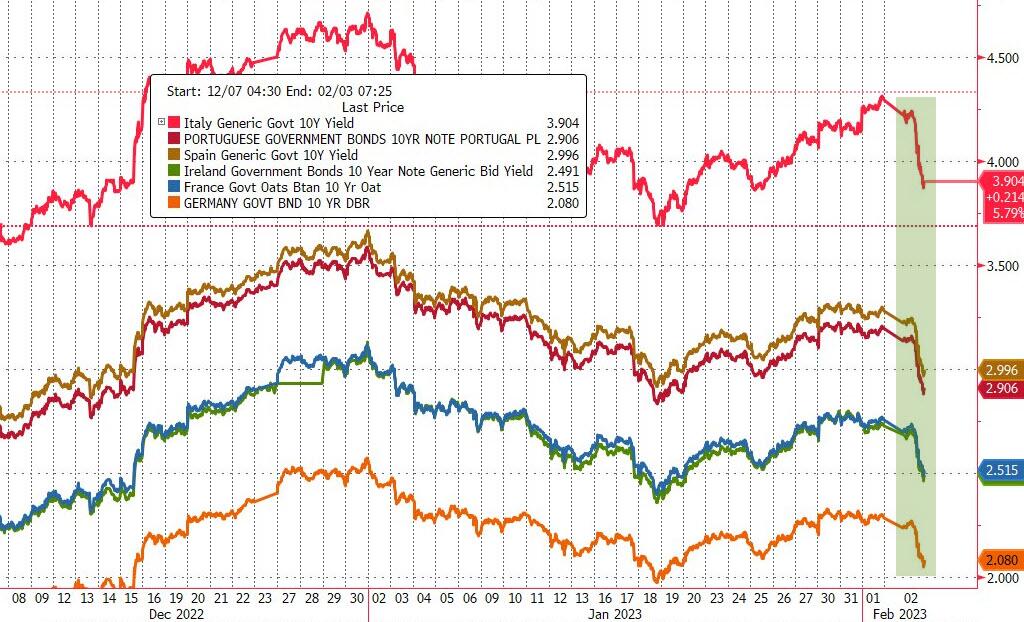

Christine Lagarde’s even easier-sounding press conference prompted a bloodbath for EU sovereign bond bears with yields collapsing everywhere…

Source: Bloomberg

And perhaps most notably, the core 10Y Bund yield crashed by the most since 2011…

Source: Bloomberg

Additionally, US Mortgage rates have tumbled for the 4th straight week to the lowest since Sept 2022…

Source: Bloomberg

The dollar retraced a lot of yesterday’s drop after the ECB was more dovish than The Fed…

Source: Bloomberg

With the Euro roundtripping the move too, ending notably lower today…

Source: Bloomberg

Bitcoin was once again rejected at $24k…

Source: Bloomberg

Gold ended the day lower – erasing all of yesterday’s gains – despite an even more dovish ECB after yesterday’s dovish Fed

And despite the exuberance about The Fed being ‘one and done’, oil prices tumbled again with WTI back to a $76 handle…

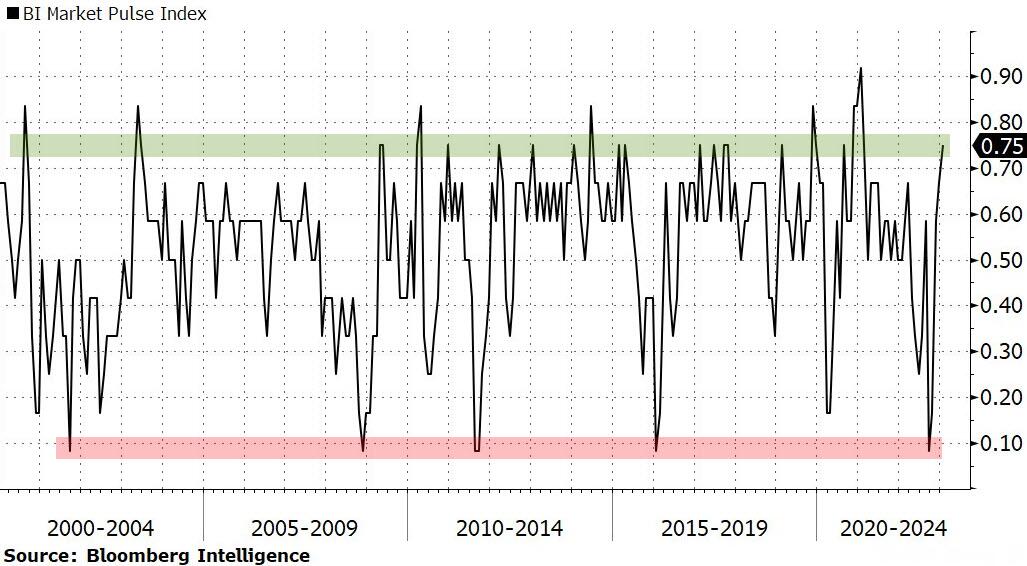

Finally, broadening participation and brightening prices improve the probability that October’s low is the one that sticks for US large-cap equities, yet signs of excessive optimism started to emerge with the January rally, Bloomberg Intelligence strategists Gina Martin Adams and Michael Casper said in a note Thursday.

The BI Market Pulse index continued its climb further into manic territory, signaling elevated risk-taking and more-volatile equity markets likely in the short term.

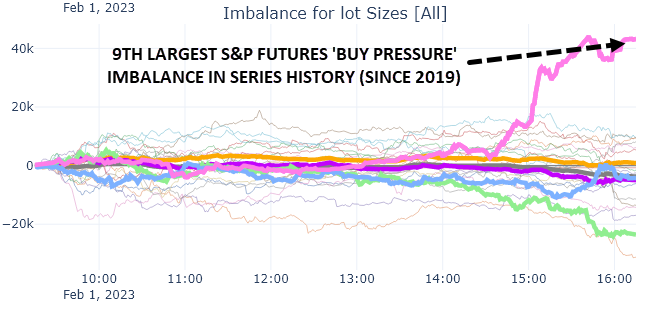

And as Nomura’s Charlie McElligott noted, the panic-grab into stocks yesterday was among the most aggressive ever…

…and historically, in the short-term, has not ended well.

Tyler Durden

Thu, 02/02/2023 – 16:02

Source link

{kind=link}