Fed Governor Waller started it with a significant reversal from his earlier dovish exuberance that helped kick off an unprecedented rally in bonds and stocks (and easing of financial conditions to end last year), but positioning The Fed’s next move as slow and steady and no rush (suggesting a March start is off the tabel and six cuts are unlikely).

Then Christine Lagarde attempted some open-mouth operations this morning from Davos, seemingly issuing forward guidance on the ECB’s actions (but notably walking back the expectations of an April cut). When asked about rate-cuts in 2024, she replied:

“I would say it’s likely too,” Lagarde said.

“But I have to be reserved, because we are also saying that we are data dependent, and that there is still a level of uncertainty and some indicators that are not anchored at the level where we would like to see them.”

Lagarde also warned that market expectations weren’t helping policy makers in their fight against inflation.

“It is not helping our fight against inflation, if the anticipation is such that they are way too high compared with what’s likely to happen.”

And then UK inflation hit, reaccelerating unexpectedly for the first time in 10 months. The Consumer Prices Index rose 4% from a year earlier in December, up from a 3.9% rise the previous month, the Office for National Statistics said Wednesday. Economists had expected a slight fall to 3.8%. Services inflation also increased, and a core measure stripping out food and energy held at 5.1%.

UK food inflation continued to slow, dropping to 8% from 9.2% in November. That was more than offset by an increase in alcohol and tobacco prices, which rose by 12.8% from a year ago.

BOE Governor Andrew Bailey has stuck to his higher-for-longer messaging on rates, warning that January’s CPI figures could show an increase due to higher household energy bills.

“The rise in inflation today suggests that the market has got ahead of itself in expecting early rate reductions,” said Ed Monk, associate director at Fidelity International.

“Today’s reading is a setback. The last portion of above-target inflation may prove the most difficult to shift.”

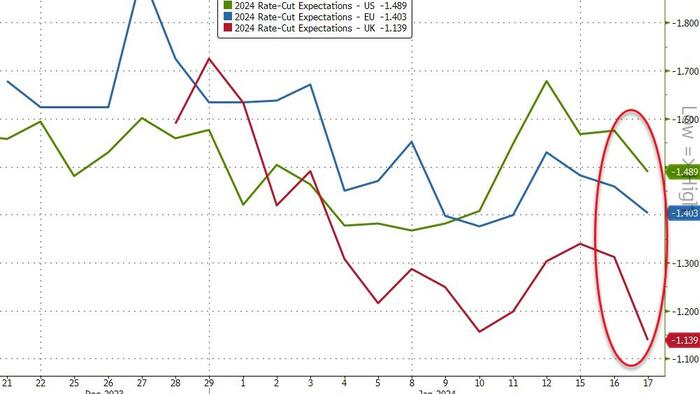

All of which sent yields higher in each region and rate-cut expectations in the US, EU, and UK are all sliding fast (most notably the latter)…

This month’s inflation figures pour cold water on the market’s ‘mission accomplished’ attitude towards central bank inflation-battling.

“Inflation was never going to be a straight line down, as we have seen in the US and Europe,” said Luke Hickmore, investment director at abrdn.

“Rates will fall this year but market expectations around when and how much are going to be very volatile.”

Stocks, bonds, and gold are all lower this morning, and the dollar stronger after this ‘hawkish’ shift.

Loading…