When the Senate unanimously passed a $2 trillion economic rescue plan late last night, it was targeting tens of millions of middle-class American households many of whom had lost their jobs, and whose lives had ground to a halt due to the global coronavirus pandemic and lockdown. It certainly wasn’t targeting Wall Street bankers.

Naturally, the Congressional stimulus plan which is set for House passage tomorrow, received much publicity – after all, some of those trillions in stimulus payments will end up going into the pockets of America’s workers, and while the final amount is a modest $1,200 per month, both Democrats and Republicans – and the President of course – will take full credit for the handout (while blaming each other for the far bigger corporate bailouts that are at the core of the package).

What has received far less coverage is that to fund this plan, the Treasury will have to issue trillions and trillions in new debt, much of which will be quickly monetized by the Fed (whose balance sheet is now $5.5 trillion and exploding), in what is essentially the arrival of helicopter money in the United States. As a result of the ongoing panic among capital markets participants who are scrambling to respond to this tsunami of new debt, there has been a surge in demand for cash and cash-equivalent products, including gold – which as we discussed earlier this week can not be found at virtually any merchant at a price remotely close to spot – and short-term Treasury Bills, those maturing in 3 months or less.

In fact, so intense is the scramble for near-term Bills that they are all now trading with a negative yield all the way to the 3 month mark, and in some cases, further out.

It is this unexpected drop in hundreds of billions in US Treasury Bills into the monetary twilight zone of negative interest rates that represents a far more secretive if far more generous handout amounting to millions in virtually guaranteed handouts to Wall Street’s bond traders.

But wait, the US doesn’t have negative yields, at least not yet, so why are Bills trading below zero. There are several answers, but the key one is traders’ preference to park cash not in their bank – which suddenly may have the dreaded “counterparty risk” thanks to some $40 billion in borrowings on the Fed’s Discount Window…

… and a bizarre surge in Libor that is hinting at one or more banks suffering from a liquidity crunch…

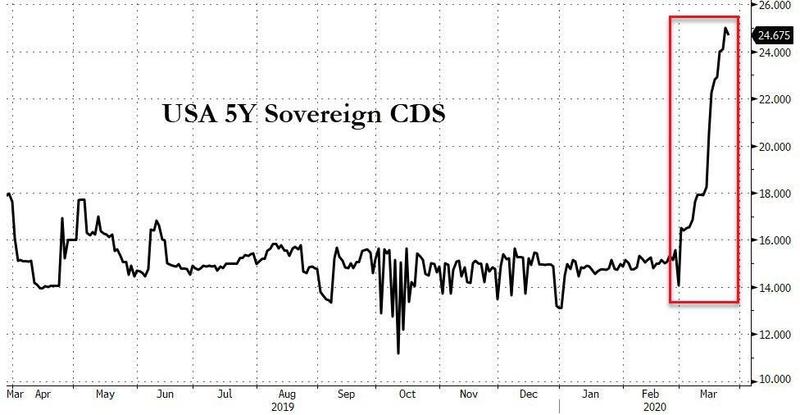

… but in the safety of debt instruments backstopped by Uncle Sam. After all, if the US were to default, which judging by the recent surge in US CDS is something quite a few are considering….

… investors would have far bigger problems than withdrawing their money.

And it is here that a fantastically profitable arbitrage has emerged, one which is far more generous to Wall Street bond traders than the fiscal bailout is to the middle class, as it is literally handing out billions in risk-free money to pretty much anyone who figures it out.

You see, unlike Germany, Switzerland or Japan, the US Treasury is prohibited from issuing debt with negative yields. Why? There is no one specific reason, but as Bloomberg, which first noticed this arb, points out “one reason the government might not want to allow negative-rate bidding is that it risks signaling to investors that negative rates are here to stay. Of course, since it is only a matter of time now before the Fed follows the ECB, BOJ and SNB by sinking into NIRP, this arb may soon disappear, but for now read on.

Effectively what the arb boils down to is taking advantage of the maximum price, or rather minimum yield limit of Bills sold to the public (but mostly to Wall Street traders) and the unlimited yields these Bills can trade in the open market.

Take the following example picked by Boomberg: on Thursday, the Treasury sold $60 billion of four-week bills at the minimum allowed rate of 0% (at a price of par, or 100 cent on the dollar).

But because the current yield on this security is roughly -0.14%, dealers can turn around and sell those bills at a premium to par, and pocket an immediate windfall of about $7 million. While that might not sound like much, with over $2.5 trillion of bills outstanding, and rolling every single month, it could add up very quickly, amounting to over $100 million every month in risk-free handouts directly from Uncle Sam if the yield on the short-end remains negative!

Another example: in addition to the four-week bill auction above, Treasury sold $50 billion of eight-week bills on Thursday at an auction rate of 0%. But in the open market, eight-week bills now trade at -0.1%, yielding a price that is above par, or over 100 cents on the dollar. (A quick BBG refresher: T-bills don’t actually pay a coupon, but are instead sold at a discount to par, which reflects the effective interest rate on the security. At 0%, the price would be 100 cents on the dollar. If the Treasury allowed negative-rate bidding, the securities would be sold at a premium.)

As Bloomberg notes, the presence of this risk-free trade “has the potential to cost U.S. taxpayers billions of dollars if rates stay lower for longer, particularly as the U.S. is poised to issue more debt after the Senate passed a $2 trillion rescue package this week.”

“The Treasury absolutely, categorically, right now has to be thinking about this,” UBS economist and a former Treasury official and adviser to the Fed, Seth Carpenter, told Bloomberg, as this trade is “essentially just transferring wealth to other people. The Treasury is in a bind and they have to make a decision on this with bill rates being negative as they are.“

Curiously, it turns out that the systems to eliminate this unprecedented arb are already in place. In 2015, when bills also traded at persistently negative levels amid supply cuts to keep the U.S. under its statutory debt limit, Treasury adjusted its systems to allow it to handle a negative auction rate, according to former Treasury officials familiar with the matter. However, according to Bloomberg, it never followed through and changed its policy.

One can only imagine why “nothing changed” in this dark corner of the Treasury market that allows bond traders to literally print free, guaranteed and perfectly legal money with the full blessing of the US Treasury. It is also hardly a surprise why virtually nobody would talk about this trade: after all if you have a golden goose, why bring attention to it?

And yet now that everyone knows about this trade, there may be little the Treasury can do to stop savvy traders from collecting millions every single day, absent permitting negative-rate bidding to eliminate the primary-secondary market arb.

As noted above, the Fed may not want to give the impression negative rates are here to stay and that negative Bill yields are just an abberation (that “explanation” may have worked before, but now that helicopter money is here, it no longer will). Then there are political considerations: while the Fed has made clear it doesn’t see negative rates as a viable policy tool, President Trump, has been pushed Powell to follow the ECB and cut its benchmark rate to below zero.

“It’s a political hot potato,” said Ward McCarthy, chief financial economist at Jefferies and a former senior economist at the Richmond Fed. And “philosophically, I am just opposed to investors paying the U.S. government to hold their debt. Especially since small investors tend to be especially involved in the Treasury bill market.”

We agree Ward, but unless you can tell us where we can buy physical gold in size and at spot, Bills it is especially once a depository institution fails and the bank runs begin: at that moment, negative yields will go well into coupon territory.

Incidentally, Bloomberg points out that this is not the first time the issue of negative-rate auctions has come up. In August 2012, in a statement presented at its quarterly debt-refunding operation, the Treasury’s then-assistant secretary for financial markets said the government was “in the process of building the operational capabilities to allow for negative-rate bidding in Treasury bill auctions, should we make the determination to allow such bidding in the future.”

Mysteriously, those capabilities never came online. Maybe because the “then assistant secretary” planned to work at a bank that is now making tens of millions from precisely this trade?

Yet even with bill demand as high as it’s been, competing priorities could keep the Treasury from pulling the trigger, at least for now.

“Selling bills at negative yields would benefit the taxpayers, but would put the Treasury at odds with the Fed, which hasn’t sanctioned negative rates,” said Mary Miller, the Treasury’s former undersecretary for domestic finance in the Obama administration, who is now running for mayor of Baltimore. The current situation “may just be a temporary disruption, so it’s worth watching to see if this rights itself with the big economic rescue steps.”

“Temporary” maybe. But what happens when, not if, the crisis returns and investors have no choice but to park trillions into the “safety” of the Bill market sending yields far below zero and on a rather “permanent” basis. Which brings up another question: just how much undisclosed taxpayer subsidies do the banks get courtesy of Uncle Sam every single day, and what happens when the current crisis fully spills over into the banking sector?