By Steven Kopits of Princeton Policy Advisors

Readers will recall that, for the last several months, I have noted that US oil production per the EIA’s weekly Petroleum Status Report was inconsistent with the data from the EIA’s monthly Drilling Productivity Report (DPR)

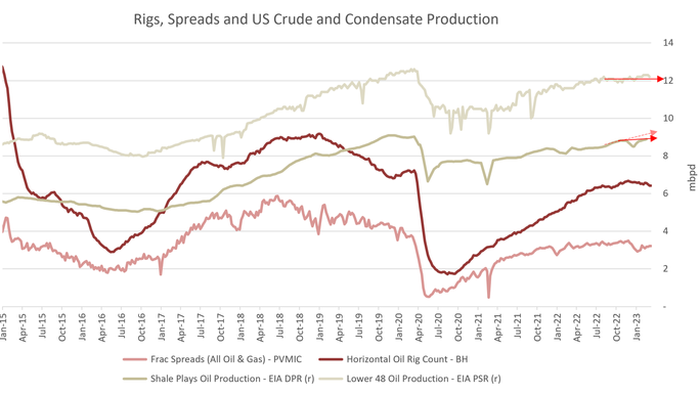

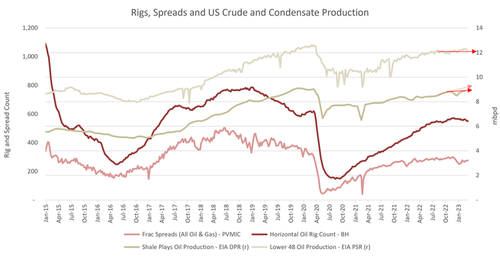

The graph below shows that state of play as of last week. The two red arrows at right show the contradictory trends, with total oil production essentially flat while shale oil production is shown rising at a healthy clip. I have noted that this contradiction would have to be resolved by either increasing the weekly numbers or reducing shale oil output.

We now have the answer.

The graph below shows the state of play as of March 14th, when the EIA issued the March DPR. It shows simply massive downward reductions in US shale oil output. In the March report, shale oil output from the key plays is reduced by 443,000 bpd for January and 250,000 bpd for February. If we go back one more month to the January DPR, shale oil production has been reduced by 542,000 bpd for December 2022. This is a huge revision, more than 4% of total US crude and condensate production over a two month period.

With this revision, as the current graph (below) shows, US shale oil production is largely flat over the last four months, and trends in shale oil supply are consistent with the overall US crude oil supply (including conventional onshore wells, Gulf of Mexico offshore, and Alaska). I need hardly point out that this is not good news, as the visible peak of horizontal oil rigs is now beginning to pair up with plateauing oil production, just as we would expect.

The most plausible interpretation is that US crude and condensate production will stagnate for the balance of the year. As I wrote in The Oil Supply Outlook (Feb. 2), the plateau has been expected since at least 2017 (see Fig. 6), so it should come as no surprise. I think the surprise, however, will be in production trends going forward. The EIA sees a long platuea in US oil production. I think it more likely that we’ll see the beginning of an erosion in supply from 2024.

In light of this, President Biden’s approval of drilling in Alaska is not hard to understand, but don’t expect it to have a material impact on supply anytime soon.

Loading…