After much bluster and jawboning, the BOJ’s repeated verbal intervention attempts to keep the USDJPY below 145 proved to be nothing but one giant bluff, at least for now.

Asian currencies – especially those like China and Japan refuse to tighten in sympathy – were already under huge pressure on Thursday after the Federal Reserve continued to tighten U.S. monetary policy when the Bank of Japan decided to counter the global tightening trend again, and stuck to its ultraloose stance.

The Japanese yen initially toyed with, then decisively weakened past 145 to the dollar, a fresh 24-year low, after the BOJ said it would maintain its monetary policy under which it is buying unlimited quantities of Japanese government bonds necessary to control the yield curve. And since the BOJ is caught in an impossible dilemma, where it can’t maintain Yield Curve Control (i.e., unlimited bond buying and thus currency printing) and a stable currency, Kuroda – whose shock and awe QE legacy is on the line, hyperinflation be damned – has again picked to sacrifice the yen which is in free fall this morning, with some speculating it could plummet as much as 147 today unless the BOJ steps in with intervention.

The BOJ announced its decision hours after the Federal Open Market Committee on Wednesday raised its key policy rate 75 basis points, or three-quarters of a percentage point, to a range of 3.0% to 3.25%, tightening for the third straight meeting, following increases June and July.

The decisions reiterated the widening gap between the Japanese central bank’s dovish policy stance and the Fed’s hawkish stance, stimulating investors to buy the dollars and sell the yen.

“We are ready to take action anytime,” said Masato Kanda, Japan’s vice finance minister for international affairs, after the yen crossed 145. “We cannot tolerate excess volatility and disorderly currency moves.” But his words this time did nothing to contain the slide, as the is sinking at an accelerating pace, much to the shock of Japanese pensioners who are not only seeing their purchasing power evaporate but are assured of importing massive inflation in the months ahead.

What happens next? According to Jun Kato, chief market analyst at Shinkin Asset Management in Tokyo, the dollar/yen could fall as low as 147 later on Thursday though the pace of yen selling is expected to slow from current levels.

The probability isn’t “zero” for USD/JPY to try its upside at the 1998 high of 147.66 later today, Kato said. “But players largely seem to have digested all the news of Fed and BOJ, and a Swiss rate hike is already factored in to limit much more upside for dollar/yen.”

Commenting on the repeated – and increasingly laughable – warnings from Japan’s top currency official Masato Kanda’s warnings which are aimed at lowering USD/JPY levels, Kato said that actual intervention is unlikely and Kanda’s comments are “nothing more than a gesture without real ammunition in store, as physical intervention can only adjust positioning and pace and will not alter a trend.” And once transitory adjustments are made, he expects the USDJPY to continue rising given fundamentals of higher US yields as the Fed makes its hawkish stance clear, adding that if the US yield curve flattens further and concerns grow more strongly about aggressive rate hikes now hurting future growth, dollar/yen may see a peak between 145-150.

Sony Financial Group agreed that there is a possibility of further rate checks by the Bank of Japan, though intervention is unrealistic: “The BOJ has conducted a rate check at 145 yen, so we are aware of that level as an upside potential,” said Juntaro Morimoto, a Tokyo-based currency analyst with Sony Financial. However, since “the gap in monetary policy between the US and Japan is widening, it is only a matter of time before it breaks through 145 yen again.” Ultimately, Morimoto sees probability of Yen at 150 against the dollar a little too far on limited room for US interest rates to rise.

Perhaps that’s true, but at this moment, the BOJ – whose bluff to intervene in the FX market has been called and the central bank has folded like a rank amateur- has effectively given the market a carte blanche to destroy the yen, especially since all those rate “checks” we read so much about proved to be just typical Japanese hot air.

The Japanese central bank conducted a foreign exchange “check” on Sept. 14, asking market participants about exchange rates. This is believed to be a move to prepare for foreign exchange intervention aimed at easing the excessive depreciation of the yen.

However, many analysts believe intervention will be next to impossible. In the case of intervention where the yen is bought and dollars sold, the maximum amount that can be used depends on the dollar cash balance in a special account for foreign exchange funds, which is under the control of the Ministry of Finance.

“As the maximum amount of foreign exchange intervention is known in advance, and [if] the BOJ decides to intervene by selling dollars and buying yen, it may inadvertently trigger speculative selling of the yen,” Masahiro Ichikawa, chief market strategist at Sumitomo Mitsui DS Asset Management, pointed out in a note.

“If the Japanese government and the BOJ are to work together to prevent the yen from depreciating, it is likely that a revision of the ultraloose monetary policy will come first, rather than currency intervention,” he added. However, in that case, “a full explanation will be required as to how the price target should be considered before the revision is made.”

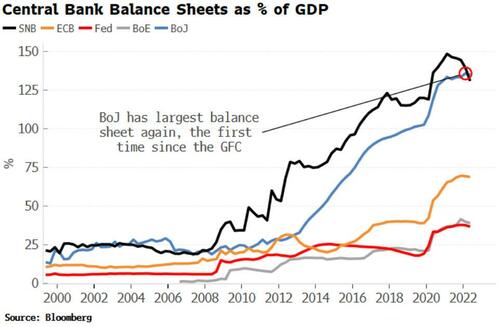

There is another reason why Kuroda is in deep fecal matter as Japan’s currency collapse accelerates: as Bloomberg notes, the Bank of Japan once again is the world’s largest central bank in GDP terms. The growing risks to financial stability will put further pressure on the bank to exit its ultra-loose monetary policy. As shown in the chart below, that mantle of the largest central-bank balance sheet was held by the Swiss National Bank since around 2007, but in recent months the SNB has been selling assets to support the franc in a bid to limit inflation.

The size of the BoJ’s balance sheet, at 135% of GDP (the real-time figure will be higher due to recent BoJ asset buying) highlights the scale of the mounting problem given the risks to financial stability.

As Bloomberg’s Simon White notes, the SNB, who are likely to raise rates later this morning, were pretty quick to change track when global inflation became a problem. They are likely to have a small sense of relief that, while their balance sheet is still large, it is now falling, and is no longer the world’s largest.